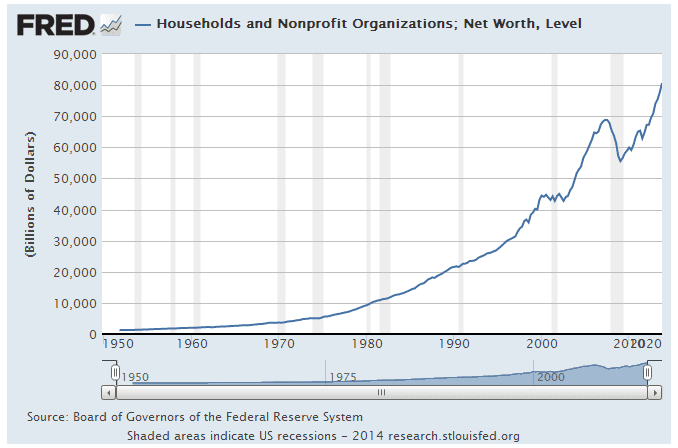

A recent Federal Reserve report shows that household finances have regained substantial ground since the Great Recession, driven largely by the run-up in home values and surge in stocks. These positive forces have contributed to the highest level of wealth in our history – the net worth of U.S. households and nonprofits reached $80.7 trillion by the end of 2013.

The effect of wealth on consumption is an issue of longstanding interest to economists, which has sparked interesting research and debate. As wealth accumulates, consumers increase confidence, and with it, consumer spending and the use of credit. Based on this reasoning, economists are anticipating further growth and gains this year.

However, not all wealth is created equal, and its impact on consumption and spending varies. Housing prices have a larger role in consumer spending compared with financial wealth like stocks and bonds. Here’s how.

Housing Prices

As home prices rise, households regain equity (they owe less on their mortgage than the value of their home). As a result, they may find it easier to sell, refinance or borrow. Overall, equity as a share of real estate has reached 51.7%, the highest point since the recession.

The key to increased spending, though, is how individuals turn rising home values into cash. How much depends on how easily individuals can borrow and the desire by banks to lend. For every dollar increase in housing values, research has estimated that consumption increases between 6 and 9 cents.

Stocks and Bonds

Stocks and bonds amount to 35 percent of net worth, and are at the highest level in 15 years. Compared with housing wealth, financial wealth is readily accessible and much easier to convert into cash. With this ease, you might think its impact on spending would be larger than housing. However, research has found just the opposite. For every dollar change in financial wealth, consumer spending tends to only increase by 2 to 4 cents.

The reduced impact of financial wealth is largely due to the fact that it is not shared as broadly as housing wealth. There are many more Americans with homes than financial investments. However, some analysts believe that the wealth and consumption relationship may not stem from the direct effect of financial wealth on spending, but rather from a signaling channel. That is, as stock prices rise and fall, household optimism about the economy may cause households to revise their expectations about their future wages and consumption.

Optimistic Expectations

In the coming months, higher home and equity values (the wealth effect) combined with the use of consumer credit, should add to the pace of consumer spending. While take-home pay remains the primary source of consumer spending, access to credit also plays a large role into economic activity.

Even though consumers have taken advantage of extremely low interest rates to purchase big ticket items, that doesn’t mean households are returning to pre-Great Recession spending habits. It appears that there is more responsible borrowing on the part of consumers. Credit card use has been extremely tepid as consumers remain hesitant to return to 2007-2008 behavior. If consumers remain hesitant, their improved finances may not lead to big gains in spending.

I remain optimistic about consumer spending this year thanks to better employment prospects, a strengthening balance sheet and an expected uptick in after-tax income that makes it easier to finance debt dependent purchases.

This optimism is tempered with the reality that rising interest rates could otherwise thwart consumer attitudes toward spending and borrowing. If interest rates begin to rise, it would make it more expensive for households to access and utilize credit and limit the increase in home prices. Alternatively, if interest rates remain steady as we expect, consumers should gain more confidence as the employment situation improves, spurring additional spending and economic activity throughout 2014.

Source: National Retail Federation

Related posts